Innovative Fintech Software Development Services

IdeaSoft is a top-notch fintech software development company that has extensive expertise in the latest tech innovations in finance and banking. Create robust and efficient software solutions for your business with our best team of dedicated fintech developers!

Who We Help

-

01

Financial Startups

Businesses that need cutting-edge fintech solutions to foster seamless user experiences, enhance security, and accelerate their performance with the best tech innovations. -

02

Retail & Commercial Banks

Finance and banking institutions that need to expand their service list, streamline and automate banking operations, and improve client service as a whole. Our FinTech application development expertise is exactly what you need! -

03

Wealth management

Businesses that need to improve profitability enable advanced data analytics and risk assessment tools that improve the money management process. We have many satisfied customers that used our FinTech software development services. -

04

Investments & family funds

Enterprises that aim to optimize investment strategies through in-depth data analytics, personalized solutions, and automated portfolio management while ensuring a seamless experience and full compliance with regulatory requirements. -

05

Insurance Providers

Businesses looking for customized and highly automated fintech products to process large volumes of data, handle policy management processes, mitigate risks, and improve customer engagement in the insurance niche. -

06

Exchanges & Brokerages

Entities that want to optimize their trading operations, increase system security, and comply with emerging industry regulations to deliver high-level services while improving their competition and profitability.

Our Financial Software Development Services

Our fintech software specialists deliver customized tech solutions that ideally cover our client’s requirements and needs. We create a robust and functional fintech product for each project to improve customer service, maximize business efficiency, and increase profitability.

-

Digital Banking Software

-

Financial Management

-

Investment & Savings

-

Stock-Trading Apps

-

Mobile Payments and Digital Wallets

-

Lending Apps

-

Crowdfunding Apps

-

Dedicated Development Teams

-

Cryptocurrency & Blockchain

-

FX Trading

Outsourcing Fintech Software

Development Services

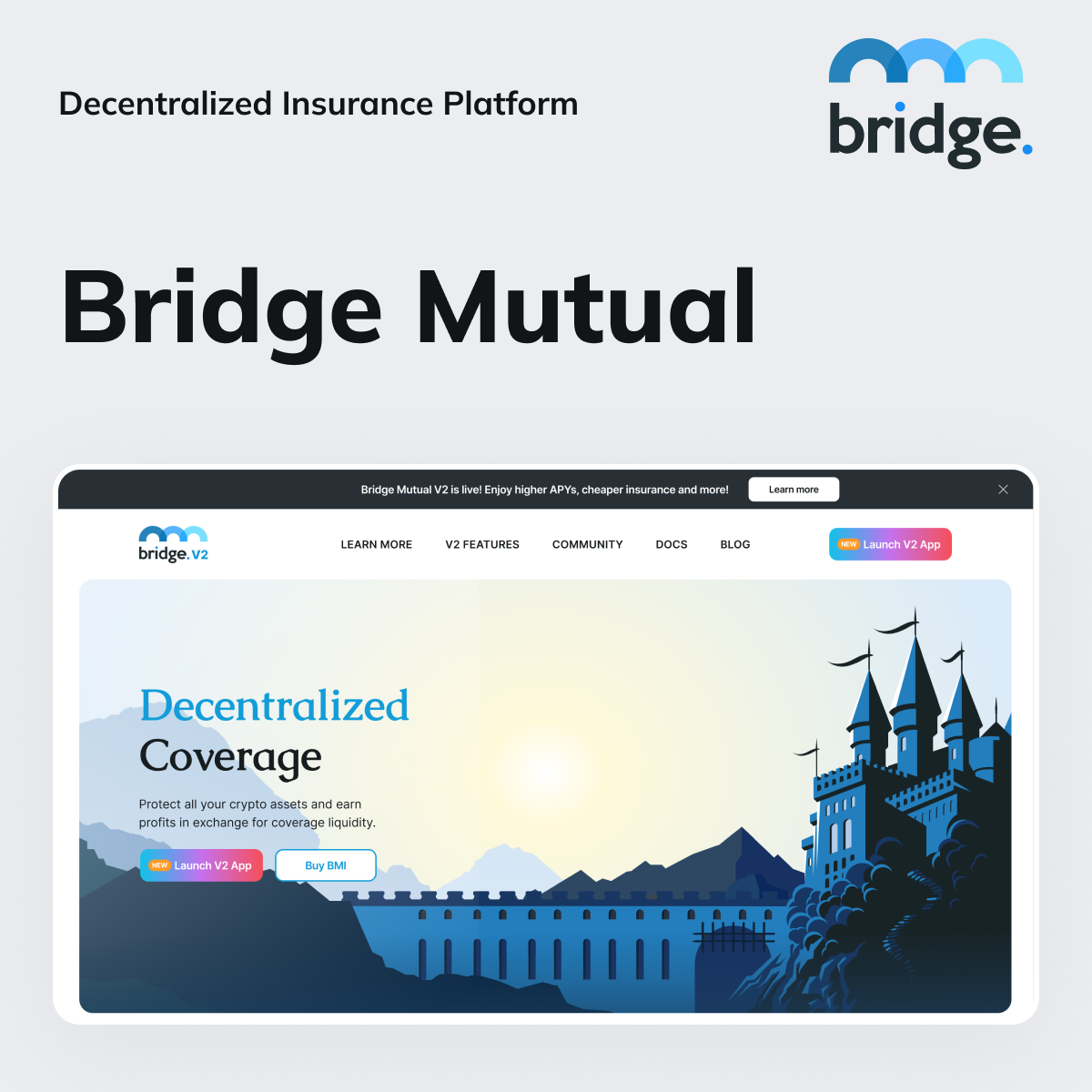

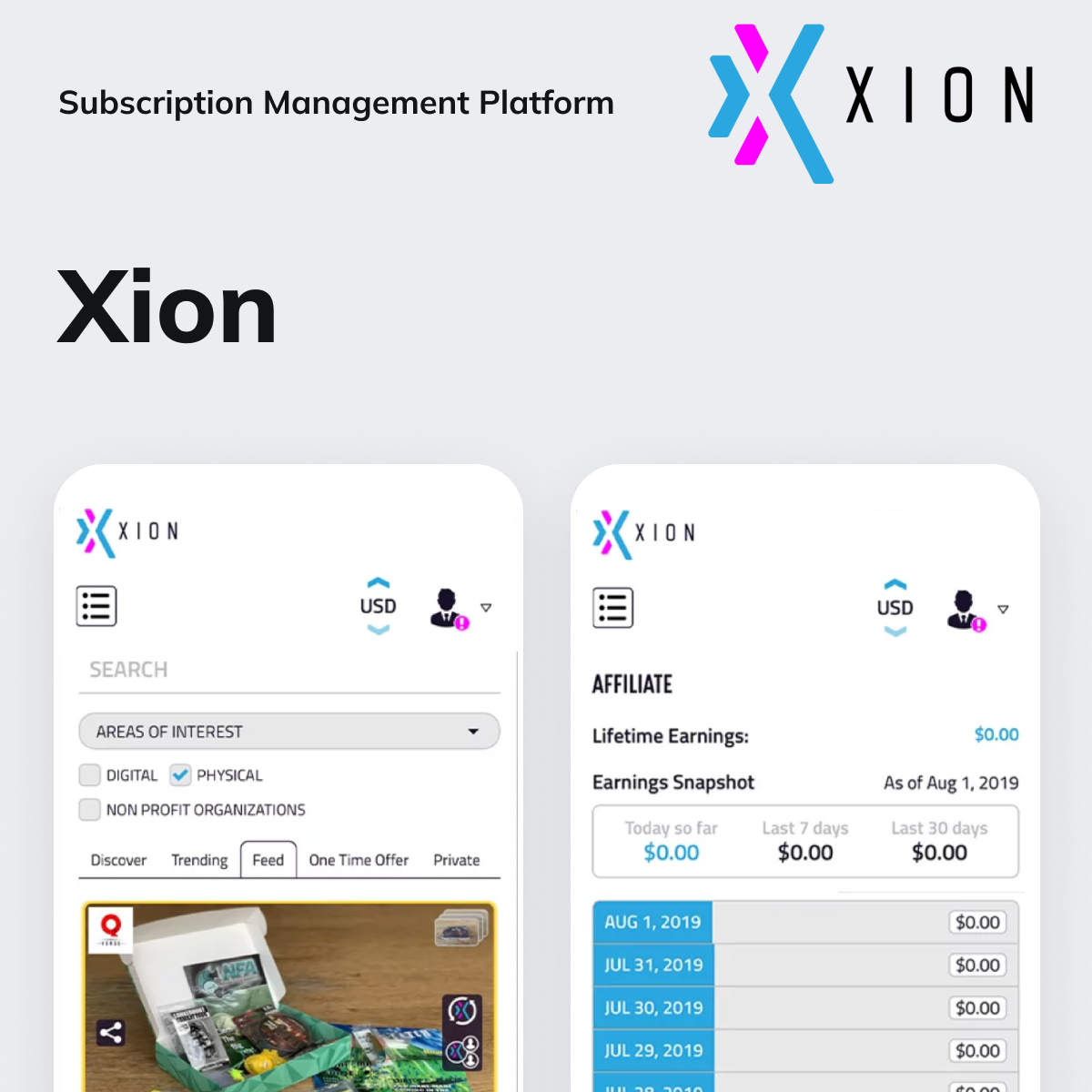

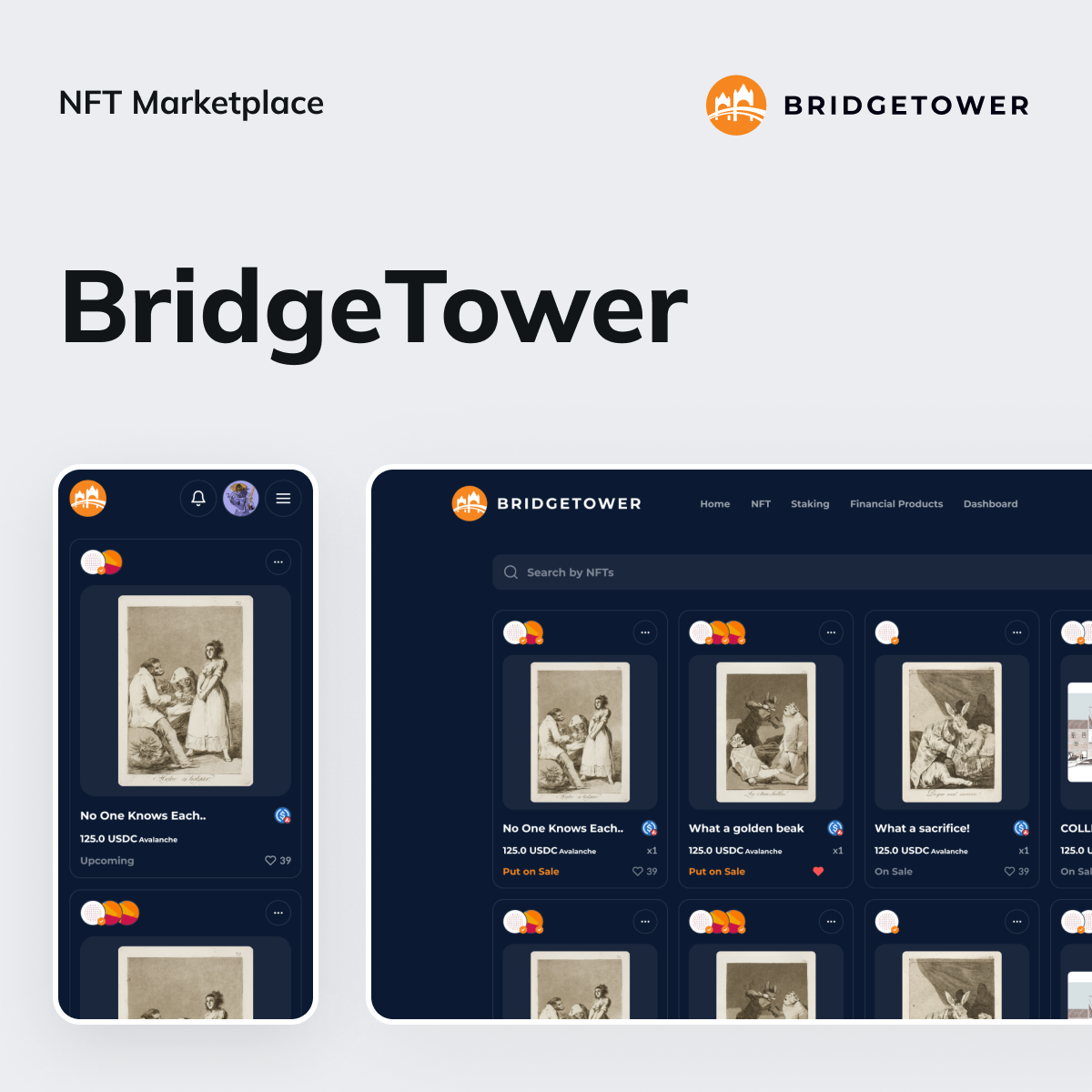

Our Success Stories

With years of expertise in fintech platforms development, the IdeaSoft team delivers top-notch fintech innovations for a wide range of companies across the globe. Whether you’re looking for fintech consulting services or need a custom fintech product for your business – we’re always here to help!

Check our portfolio of the latest fintech projects that exemplify our expertise and success in delivering high-end solutions.

Testimonials

Outsourcing Fintech Software Development Team

So much more than a company

So far, IdeaSoft has gained a reputation as a professional IT company with deep expertise in custom fintech software development. Our specialists offer progressive and powerful solutions that will ideally meet your business requirements and needs. Focused on our progress, we also actively invest in prospective ventures and join our efforts with other companies from the IT cluster to create high-end solutions for our clients.

Top 2

Fintech Developers

9+

Years on the market

250+

Successful projects

Co-founders and general partners of SID Venture Partners

Co-founders of Global Ledger

Co-founders of Orderly.Network

Founders of educational platform ICB

Our Custom Fintech Software Development Process

As a progressive fintech software development company, IdeaSoft always applies the latest tech solutions and best expertise from our dedicated managers, researchers, architects, developers, and quality assurance specialists.

Our team applies a customized agile development approach to enhance the resource efficiency of your project, facilitate its time-to-market progress and gain a competitive advantage in the target market segment.

Explore the essential stages of fintech product development that will empower your business growth.

Ideation & Planning

The success of any product is based on thorough research and detailed planning. IdeaSoft’s top experts will assess your business objectives, user pain points, and the latest industry trends to create the data-driven, custom proposal that perfectly aligns with your fintech project’s requirements and expectations.

- Analyze business pains, needs, and primary objectives

- Review the major requirements

- Review current financial ecosystem and legal landscape

- Estimate the project’s cost and delivery timeframe

- Outline the step-by-step strategy

Development & Testing

Our fintech software specialists apply the best practices in agile development to deliver a functional, efficient, and fully secure solution. At this stage, business owners are actively involved in the development process by attending the daily stand-ups and weekly meetings to guide their dev team with helpful insights and suggestions for their projects.

- Set up the team

- Build an MVP or pilot project

- Test, debug, and improve the product

- Finalize and prepare for the release

- Create detailed documentation and instructions

Delivery & Maintenance

At the final stage of the custom fintech software development, IdeaSoft specialists deliver the finalized version of your product. Our team also guarantees the ongoing support of our fintech solution, helping businesses make it more potent with the new features and optimizations on the board.

- Launch and implement the finalized fintech product

- Build the add-on features

- Support and maintain

- Ensure security & provide support

- Explore the most efficient product upgrades

Our Clients

Outsourcing Fintech Software Development Team

Frequently Asked Questions

-

Can you integrate fintech software solutions with existing systems?Yes, upgrading an existing business system with fintech development is more than possible. Once you request a consultation from a professional fintech software development company, our specialists create a fully personalized project strategy that is based on your business specifications, goals, and needs.

-

How do you ensure compliance with financial regulations?To deliver powerful custom financial software for each of our clients, IdeaSoft is actively expanding our expertise in fintech regulations. Each product we deliver is based on the most recent fintech regulation updates, existing laws, policies, procedures, and controls to ensure the best security and reliability.

-

What is your approach to fintech software development?With custom fintech software development services from IdeaSoft, our team provides comprehensive assistance across all the development stages. For each project, we conduct detailed market research and audience analysis, helping businesses choose the most relevant and efficient technologies to create a powerful solution for the fintech industry. Our clients are also actively participating in weekly meetings, and team calls during the development life cycle to track the project’s dev progress.

-

How can I get started with your fintech software development services?Whether you need to upgrade the existing banking systems or launch a custom fintech website, the key point to any project’s success is choosing the best fintech development company. The professional development team will create a personalized development strategy, covering the key market trends and your business needs to come up with the most profitable and effective solution for fintech.

-

Do you work with early-stage startups or only mature fintech companies?We collaborate with both early-stage firms and mature institutions. Our FinTech software specialists tailor FinTech solutions to your business stage to provide adaptable, scalable fintech product development support from start to launch.

-

How long does it typically take to launch an MVP for a fintech product?An MVP of a FinTech product typically takes 3–6 months, depending on complexity. Our end-to-end FinTech development services allow you to prioritize core features and achieve time-to-market. With us, you can pilot your idea cheaply and fast.

-

Can you integrate with core banking systems, payment gateways, or KYC providers?Yes, our FinTech software specialists possess in-depth experience integrating with core banking systems, payment gateways, KYC/AML systems, and third-party APIs.

-

Do you offer post-launch support or team augmentation for fintech products?Yes, absolutely. We provide full-service FinTech product development with post-launch maintenance, feature updates, and on-premises team augmentation. We can scale your FinTech solutions as your business grows.

-

How do you ensure compliance with financial regulations like PSD2, GDPR, or PCI DSS?Our end-to-end FinTech development services are compliance-centric. We integrate best practices to meet PSD2, GDPR, PCI DSS, and local regulatory standards. It is our duty to make your FinTech solutions secure and regulatory compliant from day one.